Get Started Today | Focus On Growth, We'll Handle The Numbers

When Should Architecture Firms Elect S-Corp Status?

Author: Levi Kedowide, CPA

Request a Callback

After preparing tax returns and advising over 150 S corporations (many of them architecture and professional service firms) the pattern is clear: the firms that benefit most from S-Corp election are those earning $100,000-300,000 with simple structures in tax-friendly states. The firms that regret the election are those who implemented it based on headline tax savings without calculating reasonable compensation requirements, state tax clawbacks, or whether their existing W-2 income eliminates the primary benefit

The S-Corp election benefit comes from splitting business income into two categories with different tax treatment. As a sole proprietor or default LLC, you pay 15.3% self-employment tax on every dollar of net business income:

12.4% for Social Security (up to $176,100 in 2025) and

2.9% for Medicare on all earnings,

plus 0.9% additional Medicare tax above $200,000. This happens before calculating income tax.

An S-Corp changes this by paying you W-2 salary subject to full 15.3% payroll tax, then distributing remaining profit as distributions that avoid payroll tax entirely while still being taxed as ordinary income.

The distributions aren't tax-free—they're just exempt from the 15.3% FICA specifically.

Example: $150,000 net income

As Sole Proprietor:

Self-employment tax: $22,950 (15.3% on full $150,000)

Income tax: ~$36,000 (24% bracket estimate)

Total tax: ~$58,950

As S-Corp ($90K salary / $60K distribution):

Payroll tax on salary: $13,770 (15.3% on $90,000)

Income tax on full $150,000: ~$36,000 (same)

Self-employment tax on distribution: $0

Tax savings: $9,180

But you're not pocketing $9,180 because of compliance costs:

Payroll processing: $1,200-1,800/year

S-Corp tax return (Form 1120S): $800-2,500/year

Additional administrative time

Net savings: $5,000-7,000/year

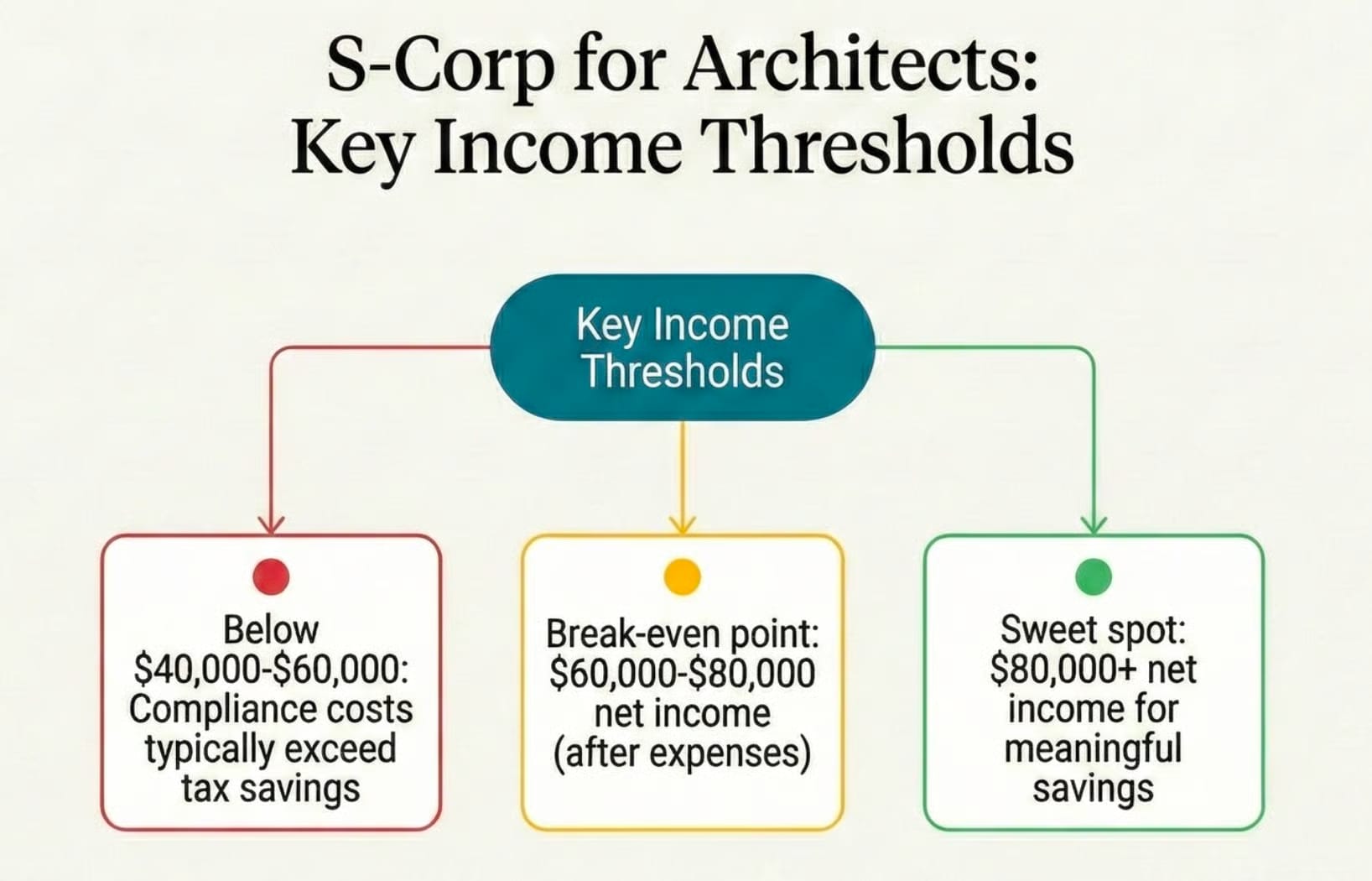

The break-even point sits around $60,000-80,000 in net income. Below this, administrative overhead consumes the tax benefit. Above $100,000, savings accelerate enough to clearly justify the complexity.

S-Corp Requirements for Architecture Firms: The Reasonable Compensation Trap

The IRS requires shareholder-employees to pay themselves fair market value for services actually performed before taking distributions. You cannot pay yourself $30,000 salary while taking $120,000 in distributions when you're personally performing billable design work the firm bills at $150-200/hour.

Reasonable compensation ranges for architects (2025):

Entry-level/recently licensed: $65,000-85,000

Mid-career licensed architect: $85,000-135,000

Senior principal, specialized practice: $120,000-180,000

Varies by market: San Francisco +30%, Nashville -15% from national median

The IRS audits S-Corps with disproportionate ratios and has detailed wage data by occupation and metro area. They flag situations where:

Distributions exceed salary by more than 2:1

Compensation falls significantly below industry norms

Professional service businesses show suspiciously round numbers ($30,000 exactly)

High profitability with inexplicably low shareholder wages

Penalties when caught:

15.3% on reclassified distributions (the tax you tried to avoid)

20% accuracy-related penalty on underpayment

Interest from original due dates

Professional fees for audit defense

Total damage: Often $25,000+ per year examined

The IRS typically examines three years simultaneously in employment tax audits, which means $75,000+ total exposure before unwinding the S-Corp structure.

When S-Corp Doesn't Work: The W-2 Income Problem

S-Corp election backfires when you're already earning W-2 wages approaching or exceeding the Social Security wage base ($176,100 for 2025). Once you've maxed out Social Security tax at your day job, additional self-employment income only faces 2.9-3.8% Medicare tax, not the full 15.3%.

The trap: As an S-Corp shareholder-employee, you must pay employer-side payroll taxes including 6.2% employer Social Security on your reasonable compensation; new money that didn't exist under sole proprietor taxation.

Example: $147,000 W-2 job + $80,000 side practice

As sole proprietor:

Social Security already maxed from W-2 job

Side practice pays only 2.9% Medicare = $2,320

Total SE tax: $2,320

As S-Corp (with $50,000 reasonable salary):

Employer Social Security on salary: $3,100 (new cost)

Medicare savings on $30,000 distribution: ~$870

Net result: Lose $2,230 by electing S-Corp

You need side practice income exceeding $200,000-300,000 annually to overcome this disadvantage. At that point you're running a full architecture firm, not a side practice.

State Tax Rules That Eliminate S-Corp Benefits

Federal self-employment tax savings disappear when state tax structures impose S-Corp-specific penalties.

States where S-Corp benefits are significantly reduced:

State | S-Corp Tax | Impact on $150K Income |

|---|---|---|

California | 1.5% franchise tax + $800 minimum | -$2,250 annual |

New York City | 8.85% corporate rate (doesn't recognize S-Corp) | Eliminates most benefit |

Tennessee | 6.5% on distributions | Claws back partial federal savings |

Texas | Franchise tax on gross receipts >$1M | Applies regardless of entity |

State Tax Rules That Eliminate S-Corp Benefits

Federal self-employment tax savings disappear when state tax structures impose S-Corp-specific penalties.

States where S-Corp benefits are significantly reduced:

State | S-Corp Tax | Impact on $150K Income |

|---|---|---|

California | 1.5% franchise tax + $800 minimum | -$2,250 annual |

New York City | 8.85% corporate rate (doesn't recognize S-Corp) | Eliminates most benefit |

Tennessee | 6.5% on distributions | Claws back partial federal savings |

Texas | Franchise tax on gross receipts >$1M | Applies regardless of entity |

California example:

Federal SE tax savings: $9,000

California franchise tax: -$2,250

Compliance costs: -$2,500

Net benefit: $4,250 (less than half the headline number)

Additional state complications:

Separate state S-Corp election required (CA Form 3560, NY, NJ, AR)

Missing state filing creates hybrid treatment: S-Corp federally, C-Corp for state

Different reasonable compensation standards in some states

State unemployment insurance and disability insurance requirements vary

For California and New York City firms, S-Corp may still justify election above $150,000 income, but benefits are substantially smaller than federal-only analysis suggests.

The QBI Deduction Impact on S-Corp Savings

Section 199A qualified business income deduction (20% of business income) works differently for S-Corps versus sole proprietors, reducing net tax benefit substantially.

Sole proprietor: 20% deduction on entire $150,000 net income

QBI deduction: $30,000

Tax savings: ~$6,600-7,200 (depending on bracket)

S-Corp: 20% deduction only on distribution portion

Salary ($90,000): No QBI deduction

Distribution ($60,000): $12,000 QBI deduction

Tax savings: ~$2,640-2,880

QBI benefit lost: $3,960-4,320 annually

This reduction comes directly off your S-Corp net savings. Combined with state taxes and compliance costs, actual benefit for $150,000 income runs $1,500-3,000 annually—meaningful but nowhere near the $9,000 headline number.

Note: QBI phases out above $191,950 (single) or $383,900 (married filing jointly) for "specified service trades or businesses" including architecture. High-income architects face additional complexity in this calculation.

S-Corp vs Partnership for Multi-Owner Architecture Firms

S-Corps require single class of stock, meaning all shareholders receive distributions proportional to ownership percentage. You cannot allocate profits based on formulas considering client origination, project management, or performance metrics.

Partnership allocation flexibility:

Three equal partners (33.3% ownership each)

Profits allocated 50%-30%-20% based on contribution

Changes annually based on performance

Special allocations for guaranteed payments

This doesn't work in an S-Corp

S-Corp restriction:

33.3% ownership = 33.3% of distributions, always

No formula-based allocation

No performance adjustments to profit splits

Salary can vary, but after-salary profit must follow ownership exactly

Workaround: Multi-entity structure where each partner has individual S-Corp contracting with partnership entity

Cost: Multiple S-Corp returns, multiple payroll systems, massive complexity

Usually not worth administrative burden for 3+ partners

Works cleanly for two equal partners, breaks down with complex structures

For architecture firms with sophisticated profit-sharing formulas or unequal contribution models, partnership taxation typically makes more sense despite slightly higher self-employment tax on guaranteed payments.

S-Corp Election Timeline and Commitment Requirements

Filing deadlines for 2026 tax year:

Form 2553 due by March 16, 2026 (75 days after January 1)

New businesses: 75 days from formation date

Late election relief available (reasonable cause required)

Retroactive election possible with proper documentation

Critical limitation: Five-year lock-in

Once elected, revoking S-Corp status creates five-year waiting period before re-election without IRS permission. You cannot:

Try it for one year and switch back

Optimize year-by-year based on income fluctuations

Convert back and forth as cash flow changes

This requires commitment that the structure makes sense for medium term (5+ years), not just current year tax optimization.

Ongoing compliance requirements:

Quarterly payroll tax filings (Form 941)

Annual W-2 preparation and filing

S-Corp tax return (Form 1120S) separate from personal return

K-1 preparation for shareholders

Corporate formalities (minutes, resolutions for major decisions)

Separate bank account and accounting records

Regular salary payments (monthly minimum, quarterly possible with justification)

Missing deadlines or failing to maintain corporate formalities can invalidate S-Corp election, triggering back taxes and penalties for all years treated as S-Corp.

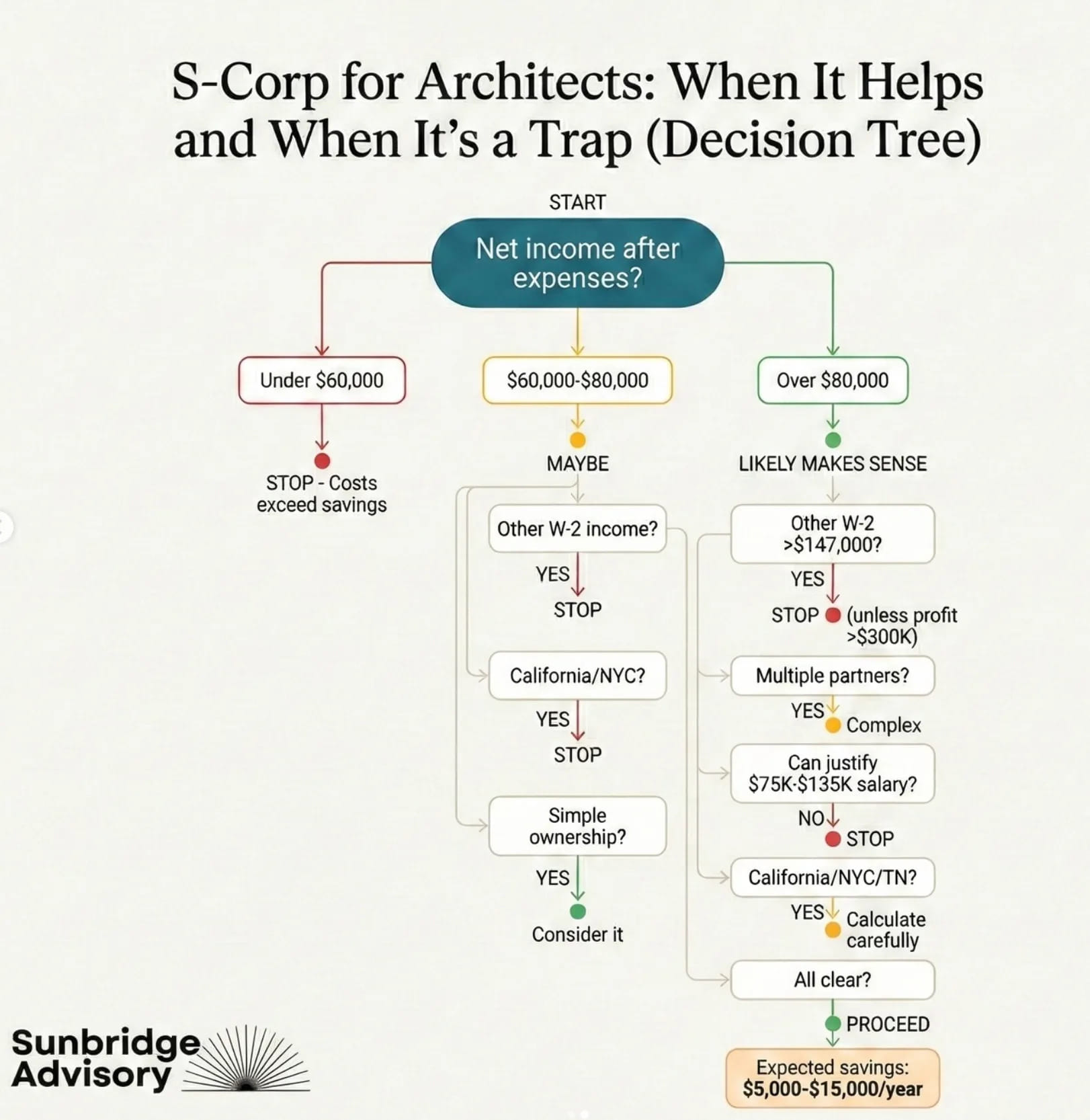

When Architecture Firms Should Elect S-Corp Status: The Decision Framework

Green light scenarios (S-Corp likely makes sense):

✓ Net income consistently $100,000-300,000+ annually

✓ Solo practitioner or two equal partners with simple arrangement

✓ No significant W-2 income from other employment

✓ Operating in tax-friendly state (Texas, Florida, most states without S-Corp specific taxes)

✓ Can justify reasonable compensation $75,000-135,000 for your market/role

✓ Leaving $40,000+ for distributions after reasonable salary

✓ Comfortable with payroll obligations and corporate formalities

✓ Planning stable structure for 5+ years

✓ Expected annual savings: $5,000-15,000 after all costs

Yellow light scenarios (requires detailed analysis):

⚠ Net income $80,000-100,000 (marginal benefit)

⚠ California, New York, Tennessee operations (state taxes reduce benefit)

⚠ Moderate W-2 income from other job ($50,000-100,000)

⚠ Partnership with straightforward equal splits

⚠ Variable income year-to-year but trending upward

⚠ Growth phase with plan to add staff

⚠ Potential savings: $2,000-5,000 annually, worth analyzing closely

Red light scenarios (S-Corp likely doesn't work):

✗ Net income below $60,000-80,000

✗ W-2 income exceeding $176,100 Social Security wage base

✗ New York City operations

✗ Three or more partners with complex allocation formulas

✗ Startup phase with unpredictable income

✗ Plans to bring in outside investors or preferred equity

✗ Can't justify reasonable compensation leaving meaningful distributions

✗ Don't want payroll administrative burden

✗ Result: Compliance costs exceed benefits, or election creates new taxes

Sunbridge Advisory

Your dedicated finance and tax team

DISCLAIMER OF TAX ADVICE: Any discussion contained herein cannot be considered to be tax advice. Actual tax advice would require a detailed and careful analysis of the facts and applicable law, which we expect would be time consuming and costly. We have not made and have not been asked to make that type of analysis in connection with any advice given in this e-mail/newsletter. As a result, we are required to advise you that any Federal tax advice rendered in this e-mail is not intended or written to be used and cannot be used for the purpose of avoiding penalties that may be imposed by the IRS. In the event you would like us to perform the type of analysis that is necessary for us to provide an opinion, that does not require the above disclaimer, as always, please feel free to contact us

Ready to take control of your finances?

Contact Sunbridge Advisory to schedule a free consultation and take control of your Finances!